Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 1

[Updated on January 30, 2025 with updated screenshots from FreeTaxUSA for the 2024 tax year.]

One of the best ways to do a backdoor Roth is to do it “clear” by contributing *for* and changing in the identical 12 months — contribute for 2024 in 2024 and convert in 2024, and contribute for 2025 in 2025 and convert in 2025. Don’t break up them into two years: contributing for 2023 in 2024 and changing in 2024 or contributing for 2024 in 2025 and changing in 2025. When you did a “clear” backdoor Roth and also you’re utilizing FreeTaxUSA, please comply with Find out how to Report Backdoor Roth In FreeTaxUSA (Up to date).

Nonetheless, many individuals didn’t know they need to’ve finished it “clear.” Some folks thought it was pure to contribute to an IRA for 2024 between January 1 and April 15, 2025. Some folks contributed on to a Roth IRA for 2024 in 2024 and solely discovered their revenue was too excessive once they did their 2024 taxes in 2025. They needed to recharacterize the earlier 12 months’s Roth IRA contribution as a Conventional IRA contribution and convert it once more to Roth after the actual fact.

While you contribute for the earlier 12 months and convert (or recharacterize and convert within the following 12 months), it’s a must to report them in your tax return in two completely different years: the contribution in a single 12 months and the conversion within the following 12 months. It’s extra complicated than a straight “clear” backdoor Roth however that’s the worth you pay for not figuring out the proper manner. This put up reveals you how you can enter the contribution half in FreeTaxUSA for the primary 12 months. Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2 reveals you how you can do the conversion half for the second 12 months.

I’m displaying two examples — (1) a direct contribution to a Conventional IRA for the earlier 12 months; and (2) recharacterizing a Roth contribution for the earlier 12 months as a Conventional contribution. Please see which instance matches your situation and comply with alongside accordingly.

Contributed for the Earlier 12 months

Right here’s the instance situation for a direct contribution to the Conventional IRA:

You contributed $7,000 to a Conventional IRA for 2024 between January 1 and April 15, 2025. You then transformed it to Roth in 2025.

As a result of your contribution was *for* 2024, that you must report it in your 2024 tax return by following this information. Since you transformed in 2025, you received’t get a 1099-R to your conversion till January 2026. You’ll report the conversion once you do your 2025 tax return. Come once more subsequent 12 months to comply with Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2.

When you contributed to a Conventional IRA in 2024 for 2023, the whole lot under ought to’ve occurred in your 2023 tax return. In different phrases, if this suits you:

You contributed $6,500 to a Conventional IRA for 2023 between January 1 and April 15, 2024. You then transformed it to Roth in 2024.

Then it’s best to’ve gone by means of the steps under in your 2023 tax return. When you didn’t, it’s best to repair your 2023 return. The conversion half is roofed in Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2.

When you’re married and each you and your partner did the identical factor, you could comply with the identical steps under for each you and your partner.

When you first contributed to a Roth IRA in 2024 after which recharacterized it as a Conventional contribution in 2025, please leap over to the following instance.

Contributed to Conventional IRA

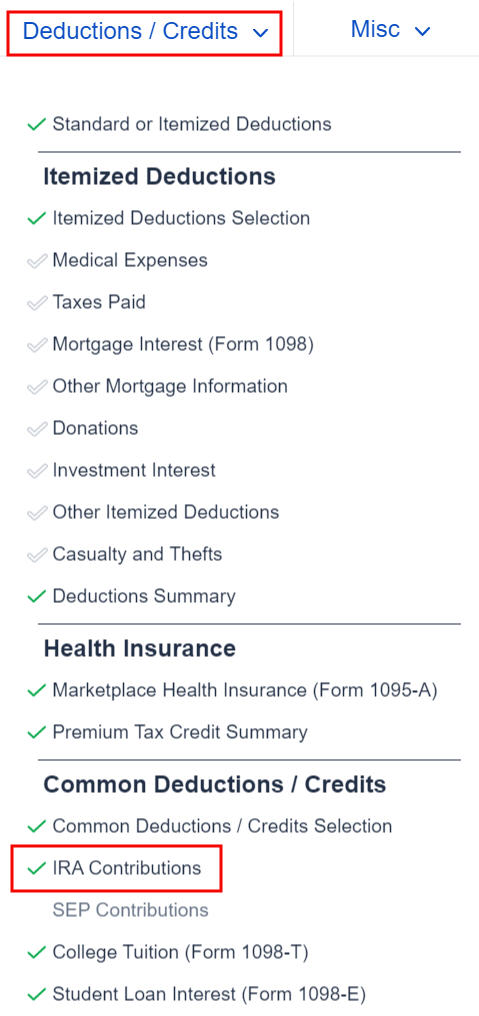

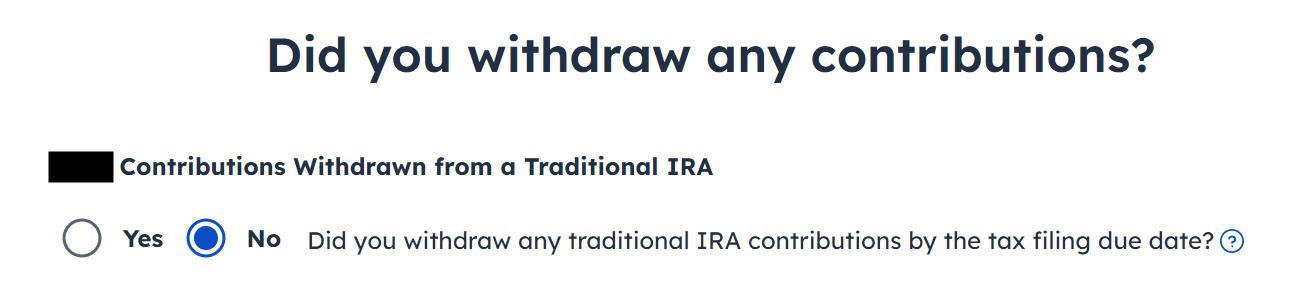

Discover the “IRA Contributions” part beneath the “Deductions / Credit” menu.

Reply Sure to the primary query although it says “throughout” 2024 once you contributed “for” 2024 in 2025. An extra contribution means contributing greater than you’re allowed to contribute. We didn’t have that.

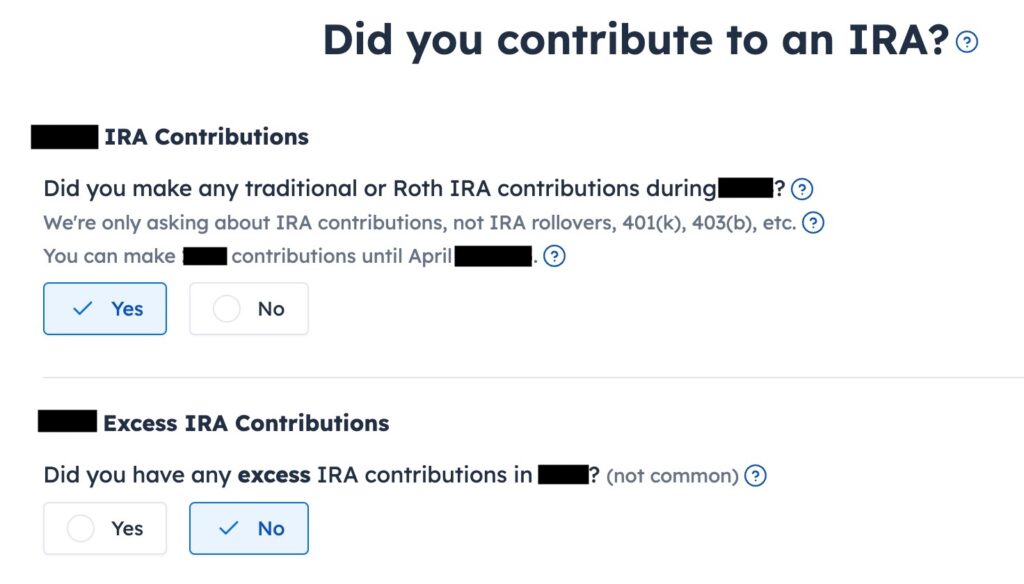

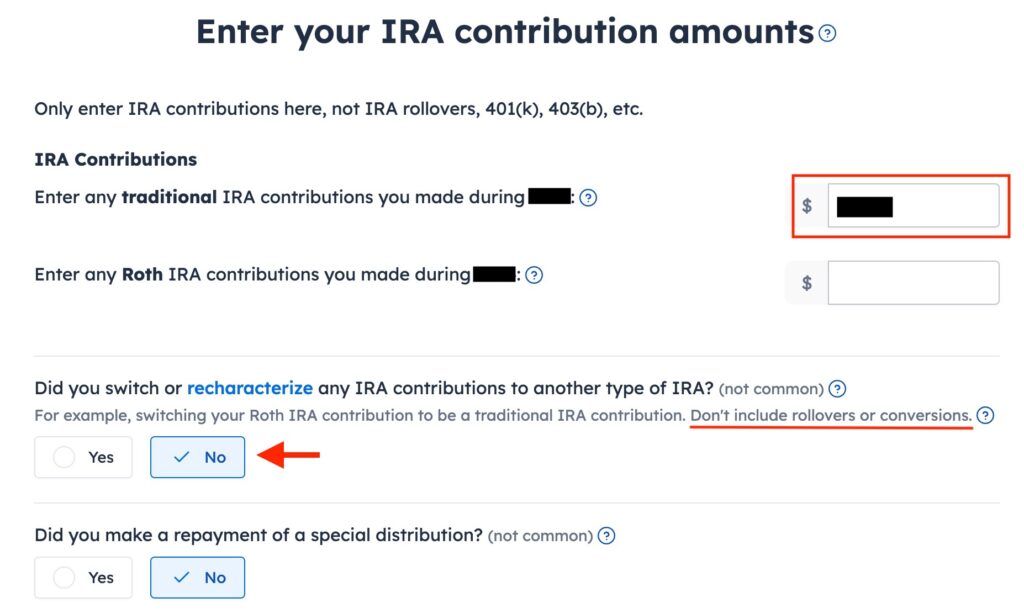

Enter the quantity you contributed to the Conventional IRA within the first field. Depart the reply to “Did you recharacterize” at No. We transformed. We didn’t swap or recharacterize. We didn’t repay any distribution both.

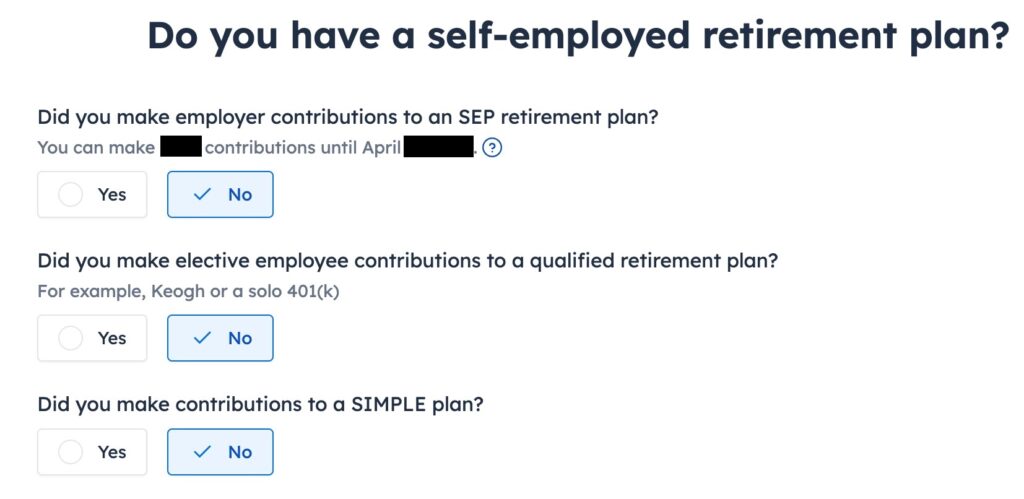

We didn’t contribute to a SEP, solo 401k, or SIMPLE plan. Reply Sure should you did.

Withdraw means pulling cash out of a Conventional IRA again to your checking account. Changing to Roth isn’t a withdrawal. Reply “No” right here.

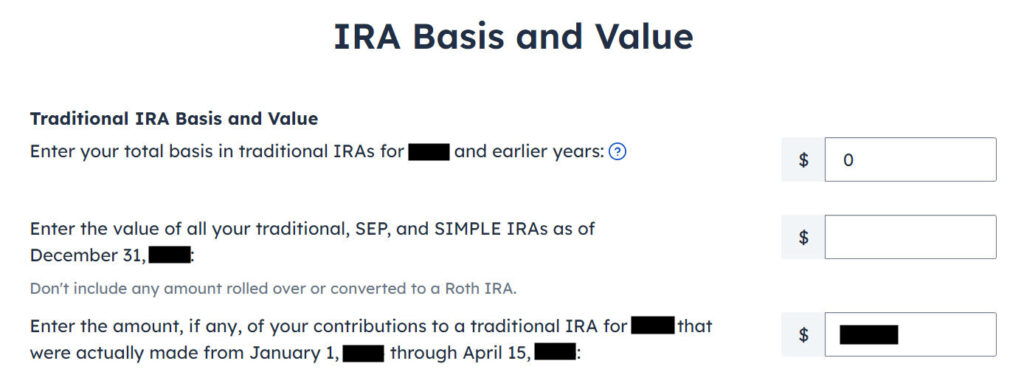

The primary field is often zero if that is the primary time you contributed to a Conventional IRA. When you made nondeductible contributions to a Conventional IRA in earlier years, get the worth out of your final 12 months’s Kind 8606 Line 14 (assuming you probably did your tax return appropriately). When you entered a quantity within the first field since you didn’t perceive what it was asking, now could be the prospect to right it.

The second field can also be clean or zero once you had no Conventional, SEP, or SIMPLE IRA as of December 31, 2024.

Enter your contribution within the third field since you did it between January 1 and April 15, 2025.

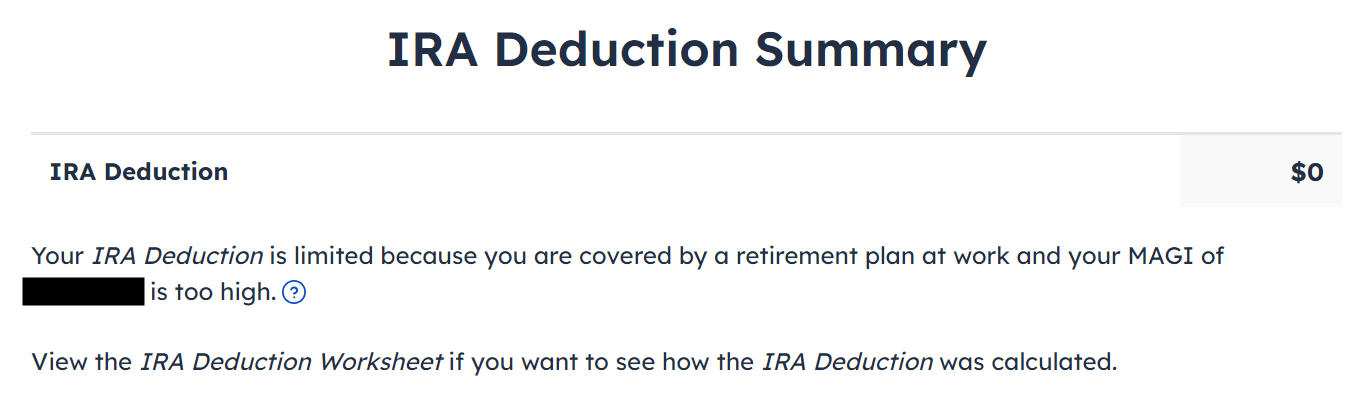

It tells us we don’t get a deduction as a result of our revenue was too excessive. We all know. That’s why we did the Backdoor Roth. If the quantity isn’t zero right here, it means the software program thinks you qualify for a deduction together with your revenue. You don’t have a alternative to say no the deduction.

Kind 8606

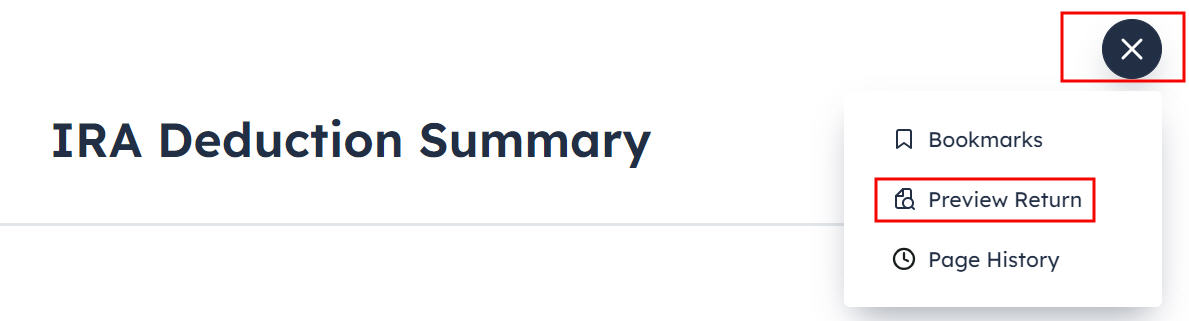

Let’s take a look at Kind 8606 to verify that it did the whole lot appropriately. Click on on the three dots on the highest proper above the IRA Deduction Abstract web page after which click on on “Preview Return.”

Scroll towards the tip of the tax varieties to search out Kind 8606. You need to see that solely strains 1, 3, and 14 are crammed in together with your contribution quantity. It’s essential to see the quantity on Line 14. This quantity will carry over to 2025. It’ll make your conversion in 2025 not taxable.

When you don’t see a Kind 8606 or in case your Kind 8606 doesn’t look proper, please test the Troubleshooting part.

Break the Cycle

Whilst you’re at it, it’s best to break the cycle of contributing for the earlier 12 months and create a brand new behavior of contributing for the present 12 months. Contribute to a Conventional IRA for 2025 in 2025 and convert in 2025.

You’re allowed to transform greater than as soon as in a single 12 months. You’re allowed to transform multiple 12 months’s contribution quantity in a single 12 months. Your bigger conversion continues to be not taxable once you convert each your 2024 contribution and your 2025 contribution in 2025. Then you’ll begin 2026 contemporary. Contribute for 2026 in 2026 and convert in 2026.

Recharacterized Roth Contribution

Now let’s take a look at our second instance situation.

You contributed $7,000 to a Roth IRA for 2024 in 2024. You realized that your revenue was too excessive once you did your 2024 taxes in 2025. You recharacterized the Roth contribution for 2024 as a Conventional contribution earlier than April 15, 2025. The IRA custodian moved $7,100 out of your Roth IRA to your Conventional IRA as a result of your authentic $7,000 contribution had some earnings. Then you definately transformed it to Roth in 2024.

As a result of your contribution was for 2024, that you must report it in your 2024 tax return by following this information. Since you transformed in 2025, you received’t get a 1099-R to your conversion till January 2026. You’ll report the conversion once you do your 2025 tax return. Come again once more subsequent 12 months to comply with Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2.

Just like our first instance, should you did the identical in 2024 for 2023, it’s best to’ve finished the whole lot under once you did your 2023 taxes. In different phrases, if this suit you:

You contributed $6,500 to a Roth IRA for 2023 in 2023. You realized that your revenue was too excessive once you did your 2023 taxes in 2024. You recharacterized the Roth contribution for 2023 as a Conventional contribution earlier than April 15, 2024. The IRA custodian moved $6,600 out of your Roth IRA to your Conventional IRA as a result of your authentic $6,500 contribution had some earnings. Then you definately transformed it to Roth in 2024.

Then it’s best to’ve taken all of the steps under final 12 months in your 2023 tax return. When you didn’t, that you must repair your 2023 return. The conversion half is roofed in Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2.

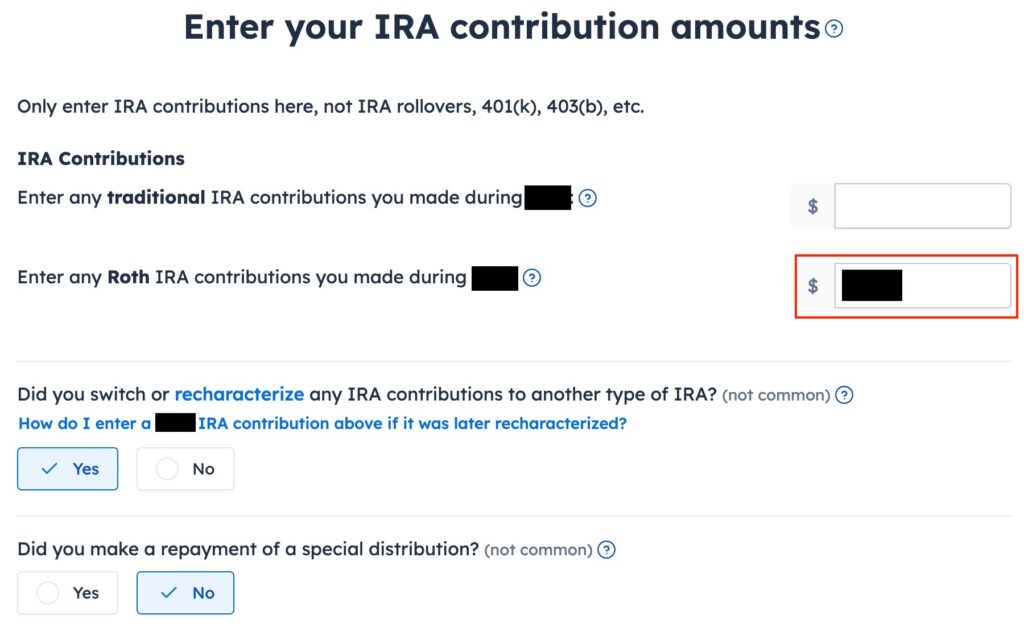

Contributed to Roth IRA

Discover the IRA Contributions part beneath the “Deductions / Credit” menu.

Reply “Sure” to the primary query. An extra contribution means contributing greater than you’re allowed to contribute. We didn’t have that.

Enter your contribution within the second field since you initially contributed to a Roth IRA. Reply “Sure” to “Did you turn or recharacterize.” We didn’t repay any particular distribution.

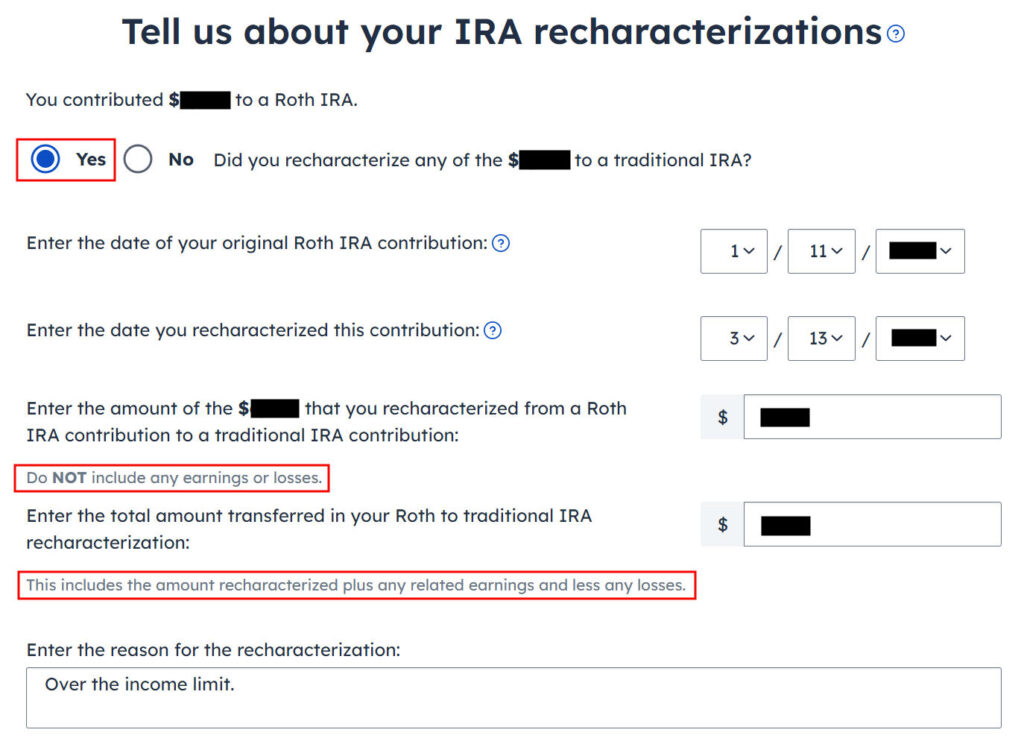

Recharacterized to Conventional

Choose “Sure” to verify you recharacterized a contribution. It opens up extra inputs for a press release required by the IRS. When you recharacterized 100% of your authentic contribution, enter it within the first field. It’s $7,000 in our instance. We enter $7,100 from our instance within the second field, which is the quantity that the IRA custodian moved from the Roth IRA to the Conventional IRA once we recharacterized.

We didn’t contribute to a SEP, solo 401k, or SIMPLE plan. Reply Sure should you did.

Withdraw means pulling cash out of a Conventional IRA again to your checking account. Changing to Roth isn’t a withdrawal. Reply “No” right here.

All three packing containers ought to usually be clean or zero.

The primary field is often zero once you didn’t make any nondeductible contributions to a Conventional IRA in earlier years. When you did, get the worth out of your final 12 months’s Kind 8606 Line 14 (assuming you probably did your tax return appropriately). When you entered a quantity within the first field since you didn’t perceive what it was asking, now could be the prospect to right it.

The second field can also be clean or zero once you had no Conventional, SEP, or SIMPLE IRA as of December 31, 2024.

The third field can also be clean or zero since you made the unique contribution in 2024. Recharacterizing makes it as should you contributed to a Conventional IRA to start with.

It tells us we don’t get a deduction as a result of our revenue was too excessive. We all know. That’s why we did the Backdoor Roth. If the quantity isn’t zero right here, it means the software program thinks you qualify for a deduction together with your revenue. You don’t have a alternative to say no the deduction.

Kind 8606

Let’s take a look at the Kind 8606 to verify that it did the whole lot appropriately. Click on on the three dots on the highest proper above the IRA Deduction Abstract after which click on on “Preview Return.”

Scroll towards the tip of the tax varieties to search out Kind 8606. You need to see that solely strains 1, 3, and 14 are crammed in together with your contribution quantity. It’s essential to see the quantity in Line 14. This quantity will carry over to 2025. It’ll make your conversion in 2025 not taxable.

When you don’t see a Kind 8606 or in case your Kind 8606 doesn’t look proper, please test the Troubleshooting part.

Swap to Clear Backdoor Roth

While you’re at it, it’s best to swap to a clear backdoor Roth for 2025. Relatively than contributing on to a Roth IRA, seeing that you simply exceed the revenue restrict, recharacterizing it, and changing it once more, it’s best to merely contribute to a Conventional IRA for 2025 in 2025 and convert it to Roth in 2025 if there’s any risk that your revenue might be over the restrict once more.

You’re allowed to do a clear backdoor Roth even when your revenue finally ends up under the revenue restrict for a direct contribution to a Roth IRA. It’s a lot less complicated than the complicated recharacterize-and-convert maneuver.

You’re allowed to transform greater than as soon as in the identical 12 months. You’re allowed to transform multiple 12 months’s contribution quantity in a single 12 months. Your bigger conversion continues to be not taxable once you convert each your 2024 contribution and your 2025 contribution in 2025. Then you’ll begin 2026 contemporary. Contribute for 2026 in 2026 and convert in 2026.

Troubleshooting

When you adopted the steps and you aren’t getting the anticipated outcomes, right here are some things to test.

No 1099-R

You get a 1099-R provided that you transformed to Roth in 2024. Since you solely transformed in 2025, you received’t get a 1099-R till January 2026. That is regular. You do the conversion half subsequent 12 months through the use of Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 12 months 2.

Contribution Is Deductible

When you don’t have a retirement plan at work, you have got a better revenue restrict to take a deduction in your Conventional IRA contribution. FreeTaxUSA gives you the deduction if it sees that you simply qualify. It doesn’t provide the alternative of creating it non-deductible. You see this deduction on Schedule 1, Line 20.

You don’t get a Kind 8606 when your contribution is absolutely deductible. The numbers on Traces 1, 3, and 14 of your Kind 8606 are lower than your full contribution when your contribution is partially deductible.

Taking this deduction additionally makes your Roth IRA conversion taxable subsequent 12 months. You’ll pay much less tax this 12 months and extra tax subsequent 12 months. In a manner, it’s higher since you get to make use of the cash for one 12 months.

When you even have a retirement plan at work, the software program didn’t see it. Whether or not you have got a retirement plan at work is marked by the “Retirement plan” field in Field 13 of your W-2.

Perhaps you forgot to test it once you entered the W-2. Double-check the “Retirement plan” field in Field 13 of your (and your partner’s) W-2 entries in FreeTaxUSA to verify they match the W-2.

Say No To Administration Charges

In case you are paying an advisor a proportion of your belongings, you’re paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

Leave a Reply